Monetary policy, exchange rate and taming inflation

Mamun Rashid

Mamun Rashid

The Monetary Policy Statement (MPS) for the second half of fiscal 2011 is focusing on a continuous watch towards locating and neutralising likely inflationary pressures from the growth-supportive monetary and credit policies.

The policy has taken a stance to extend credit to agriculture, small and medium enterprises (SME), rural economy, housing loans, shipbuilding, and rural energy. This stance is backed by the reasoning that the domestic economy is operating below capacity and expansionary policy in the targeted sector would help to bring in short term stability and to realise long term growth prospects.

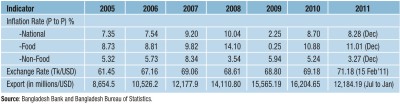

While we welcome that, the common people seem to be confused about some of the Bangladesh Bank (BB) stances. The dollar rate has gone up significantly, making import apparently much costlier than before and at times, there are serious issues coming up with regard to timely settlement of import liabilities due to foreign currency (FCY) liquidity shortage in the market. The central bank in the recent past was supporting essential commodity imports, especially in the state sector by supplying FCY liquidity to them. Lately, they expressed their shyness in continuing that and instead, they are allowing a few commercial banks to overdraw their FCY accounts held with the central bank.

However, this is creating serious disconnect in managing banks' asset and liabilities, especially in a fluctuating market, and banks are being forced to get into a tussle with their esteemed clients. Besides, common people on the streets cannot reconcile high dollar prices with a higher FX reserve. Their confusion heightens when they see imported items getting dearer, creating serious disengagement with the government's election pledges.

A study by BB in the past suggested a nominal US dollar over-valuation against the taka when compared to nominal effective exchange rate (NEER) and real effective exchange rate (REER). The monetary policy therefore emphasised stability of the exchange rate to maintain external competitiveness. However, with almost 6 percent depreciation of taka against dollar, now that gap has narrowed a lot, if not gone.

There are impending debates among economists (usually banks or bankers do not dare to criticise the central bank in emerging countries like Bangladesh), whether BB should try to dampen the dollar rate to support price reductions of imported essentials. Their argument in favour of an appreciated taka is emanating from an emerging debate of export being increasingly becoming insensitive to the exchange rate, rather more dependent on labor wages, productivity and an efficient supply chain.

The world has been experiencing an episode of inflation in commodity and fuel prices for quite some time and now it is only following one way traffic of going up, while the domestic inflationary pressure is reportedly making the life of the poor, low-, and middle-income people somehow miserable.

Had the Bangladesh currency been appreciated in terms of its intervention currency, that is, the US dollar, the costs of all imports, including essential commodities, would have gone down to some extent. That would have been considered otherwise a welcome development. In that event, the government could be in a better position to blunt the edge of all public criticisms for its failure to rein in soaring prices. The consumers could also see some sort of relief. However, policy planners as well as 'inflation targeting group' with the partner agencies feel, monetary management tools in their entirety cannot control the price rise. Rather, governments need to come up with fiscal measures (including safety net or targeted subsidy) to help the marginalised groups, without denting the growth driving sectors.

They also feel that appreciation of the taka is easier said than done. If the value of the US dollar depreciates against the taka, it would take its toll on the export sector, that is, the lifeline of the economy. There could also be cuts in employment in all export-oriented sectors. A strong taka will also have the potential of affecting the flow of inward remittance by the non-resident Bangladeshis through official channels and thereby, put further pressure on our widening balance of payment.

The government reported to have initiated a dialogue in reference to taking a balance of payment support fund of $1 billion from International Monetary Fund (IMF), which they have done at various intervals in the past, especially with a heated external sector, crop loss due to natural calamities or international food price surge.

Bangladesh had its first sovereign credit rating by Standard & Poor's as well as Moody's in the recent past and the rating came out to be quite good vis-à-vis peer countries. Analysts felt it was the best time for us to go into international markets to raise some money through sovereign bonds, like similar countries. That would have helped us support growth financing or at least try Bangladesh's ability to raise money from global markets and avoid at-times undesirable and conditional IMF support.

Take it or leave it, the Bangladesh economy has become more integrated with the world over last one and half decade. Thus, it is hard to insulate commodities prices in the domestic market from global influences. What is more important is that there is no guarantee that traders would be selling goods at prices lower than existing levels, in spite of the benefits to be accrued from a possible appreciation of the taka.

So, upward adjustment of the taka against the US dollar remains a dilemma for the central bank. However, the government and the central bank need to use whatever tools they have, under their control, to tame soaring inflation without compromising on growth.

There needs to be a good balance between monetary and fiscal policy execution. While the fiscal policy would be targeted at equitable distribution and adequate safety nets for the marginalised, the monetary policy would focus on price stability.

Unless we bring transparency in goal setting for fiscal and monetary policies, they would remain ineffective in our endeavor to fight international economic uncertainties and spikes in the domestic economy.

The writer is an adjunct professor at NSU Business School and can be reached at mamun1960@gmail.com.

News: The Daily Star/ Bangladesh/ Mar-02-2011

Comments